If you think getting a mortgage is as easy as qualifying based on your lender’s mortgage rate, think again! You have to pass a test; A stress test.

What is the mortgage stress test?

This is what the Office of the Superintendent of Financial Institutions says (OFSI) says1

“One tool that OSFI requires institutions to use is the minimum qualifying rate (MQR) – also known as the “stress test.” This and other expectations are set out in OSFI Guideline B-20 that federally regulated lenders are required to follow when granting an uninsured mortgage.

The MQR tests a borrower’s ability to continue to make their mortgage payments in the event of difficult economic circumstances including a rise in interest rates, fluctuating house prices, or a reduction of income such as an on the job injury or job loss.

By qualifying borrowers at a higher interest rate than the actual rate they have agreed to with their lender, OSFI is ensuring that lenders remain prudent and responsible with their lending practices. By insisting on these sound mortgage underwriting practices, OSFI creates a built-in margin of safety that strongly contributes to the soundness of Canada’s financial system.”

The federal government requires you to pass this test if you’re borrowing from any federally regulated lender (such as Canada’s major banks, as well as lenders who use CMHC’s products), to ensure that you could afford increases in lending rates.

In other words: If rates go up, would you still be able to afford to make their payments?

The rationale is that the test would protect borrowers and lenders from a disastrous situation where borrowers started to default on their mortgage payments, (not make their payments), due to rising rates. This would lead, theoretically, to lenders having to sell the properties of defaulting borrowers, potentially flooding the market with properties that would effectively create more supply than demand, and ultimately causing a housing market crash.

So, this was a pre-emptive move to reinforce the stability of the mortgage and housing markets, and protect CMHC from having to pay out more claims to lenders.

Well, it seems to have paid off.

As Ben Gully, Assistant Superintendent, Regulation at OSFI said, “In a complicated and sometimes volatile housing market, the need for sound mortgage underwriting cannot be underestimated. The rate in place as of June 1, 2021 will help support financial resilience should economic circumstances change, while our commitment to review the qualifying rate at least annually will contribute to continued confidence in the Canadian financial system.”

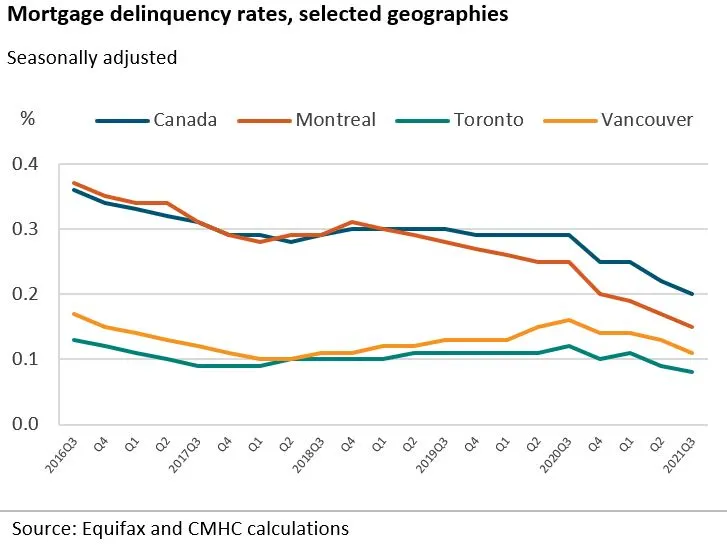

Since Q3 of 2016, mortgage delinquency rates have dropped from 0.36% to 0.2% nationally, as the chart provided from CMHC (below) indicates. Decreases have been seen in all major markets.

Interestingly, in the hottest markets in Canada, (Toronto and Vancouver), rates are the lowest, at 0.08 and 0.11, respectively.

Lessons to Be Learned

It appears that we need the government to force us to be responsible with our money. Or do we? Delinquency rates were already incredibly low and the stress test helped push them lower. Was the government right in its proactive approach to staving off a credit crisis?

The truth is we’ll likely never know. But that’s not a bad thing! If they did nothing and the market collapsed or borrowers started getting into trouble, many would have blamed them for inaction. Since they were proactive, there’s nothing to blame them for because the issue they tried to prevent never happened. It was prevented.

Of course, this is conjecture. We don’t know that issues were imminent, nor do we know if this step prevented anything. But at least it was leadership. Good or bad is up to you to decide.

Impact on Current Borrowing[1]

Let’s have a look at how the stress test impacts the borrowing power of someone today.

Currently, the minimum qualifying rate, as set by OSFI (Office of the Superintendent of Financial Institutions), is 5.25%, or the rate your lender is offering plus 2%; whichever is higher.

If we use the TD Broker Rate of 2.49% for a 5-year Fixed term, a borrower earning $100,000 would be able to borrow $614,569. Based on the stress test rate of 5.25%, the same borrower would be limited to borrow $461,473. For this borrower to be able to afford that $614,569 they’d need to earn an additional $912 per month, or $10,944 per year.

As we can see, those are significant differences.

Want to calculate your maximum mortgage amount yourself? click here to use the Government of Canada’s calculator

What to do?

Talk to a licensed mortgage agent or broker. They’ll be able to help you navigate these convoluted waters. (Want to learn how to become one? Just click here)

Why?

Because mortgage agents and brokers have access to lenders that you don’t, including lenders that don’t have to use the stress test! These lenders include alternative lenders and provincially regulated credit unions.

Coupled with increased down payment requirements, soaring property values and a looming interest rate increase, speaking to the most qualified professionals in the industry is, in my opinion, a must.

Cheers,

Joe White,

President, Real Estate and Mortgage Institute of Canada Inc.

[1] Assumptions: $100/mth for heat; $400/mth for property taxes; SAGEN GDS of 39%; monthly mortgage payment of $2,750;no debts impacting the TDS;